{kind=link}

Leon Neal

Fortune favors the courageous.

That quote is definitely from Matt Damon from his widely-despised Crypto.com (CRO) business from late 2021. Crypto.com is just not Coinbase (NASDAQ:COIN) however the sentiment nonetheless applies. Although at the moment it was shoppers who had been “courageous” when plowing fiat into Shiba Inu (SHIB-USD) and different dog-themed joke coins. Now it is all about Bonk (BONK-USD), the new dog money that everybody appears enthusiastic about. We all know how the Bonk story will possible finish. This time although it is seemingly traders within the very enterprise of crypto who have to be courageous as shopping for COIN at the moment could be shopping for shares of an organization that appears like a sinking ship. With so many apparent rip-off crypto cash and currencies, the rational query is what sort of regulatory wrath awaits this business?

Regulatory Sport Idea

Let’s begin with a easy query; can the U.S. authorities ban the usage of crypto? The reply I’ve come to for years might be not in a manner that’s truly enforceable. Crypto can very simply be criminalized however legal guidelines do not finally cease folks from turning into criminals once they need to break the foundations. Look no additional than the latest FTX disaster (FTT-USD) or any monetary fraud all through historical past. Firms like Coinbase might finally survive crypto winter whether it is within the curiosity of the US federal authorities that they do.

The choice is all crypto buying and selling exercise strikes on-chain the place, regardless of the clear nature of a public ledger, it would possible be more durable for the IRS to affiliate positive factors immediately with Social Safety numbers. In the end tax income is what issues and that’s what is probably going the actual motivation behind the not too long ago proposed Digital Asset Anti-Cash Laundering Act. It’s attention-grabbing that after the failure of a centralized crypto custodian marketed because the “trusted” change, fairly than pointers for higher proof of reserves transparency from custodians, the push from some within the authorities has as an alternative been to make it extra onerous for self-custody wallets to do enterprise. From CoinDesk:

If it turns into legislation, the Digital Asset Anti-Cash Laundering Act will carry know-your-customer (KYC) guidelines to crypto members comparable to pockets suppliers and miners

KYC guidelines for pockets suppliers would primarily make any self-custodial pockets utility that does not gather private identification data like bodily addresses and driver’s license knowledge not compliant with the legislation. From the place I sit, this might imply that self-custody functions like Trust Wallet (TWT-USD) must begin accumulating and reporting person knowledge with the federal authorities. It’s extremely unlikely that any or most of those functions would have the ability to do such a factor. A lot of them are constructed with open-source software program and are maintained by volunteers.

To be clear, I am not saying the Digital Asset Anti-Cash Laundering Act is prone to cross or that it ought to cross. But when it does cross, it is most likely excellent news for centralized exchanges. Since there are quite a few regulatory considerations about Binance (BNB-USD), I feel the largest beneficiary of extra crypto-centric regulation would finally be Coinbase. Nonetheless, predicting what Washington will do is troublesome and never the principle purpose why COIN seems attention-grabbing at the moment.

Brief Squeeze Setup

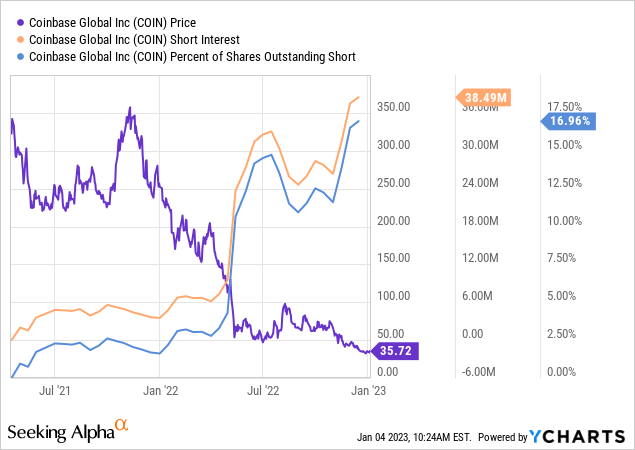

The extent of shorting that has taken place in Coinbase has been substantial. Based on the final quick curiosity report, COIN has 38.5 million shares quick – primarily 17% of the shares excellent and 21% of the float.

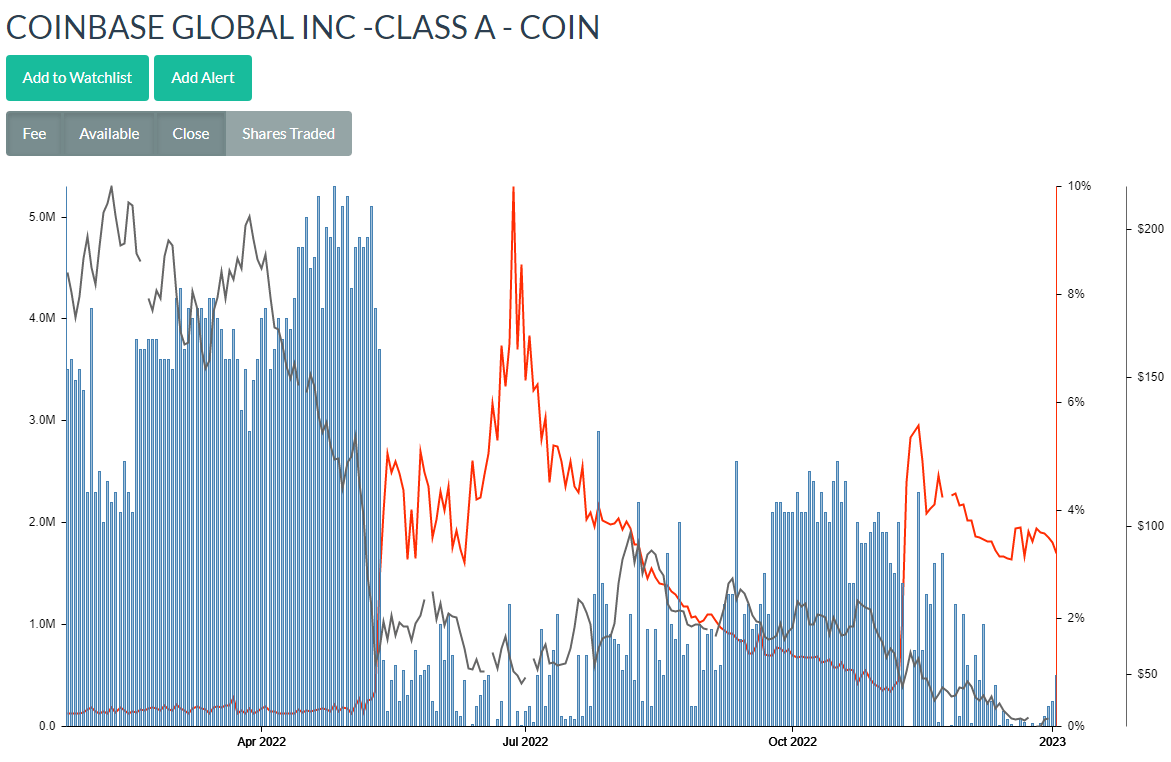

Brief sellers have completed extremely properly with Coinbase since $400 – it is actually been a outstanding commerce. However I’ve to marvel if the commerce has turn into too one-sided at this level. Trying on the iBorrowDesk knowledge reveals a inventory that could be very costly to borrow at present with not many shares obtainable left to promote:

iBorrowDesk

And this has truly been the case for a very long time. COIN’s shares obtainable to quick have not touched pre-LUNA (LUNC-USD) collapse highs. Not solely that, however the borrow price has been extraordinarily elevated as properly. There’s severe squeeze potential on this identify proper now for my part. In my expertise, quick curiosity ratios this excessive are typically for dying retail chains and firms which can be clearly going bankrupt. I can not get there on Coinbase as a result of the stability sheet does not but mirror an organization knocking on loss of life’s door.

Steadiness Sheet and Valuation

Now we have to caveat these metrics as a result of they’re the most recent numbers we now have they usually pre-date the FTX collapse. The property held for purchasers are possible a lot decrease than they had been on the finish of Q3 however in response to the final submitting these had been liabilities that had been over-collateralized.

| Q3-22 | |

| Money and ST Investments | 5,009.10 |

| Complete Present Property | 107,680.00 |

| Complete Property | 111,168.40 |

| Complete Present liabilities | 102,073.10 |

| Lengthy-Time period Debt | 3,391.20 |

| Complete Liabilities | 105,542.00 |

| Internet Debt | -1,324.50 |

Supply: In search of Alpha, figures in tens of millions of U.S. {dollars}

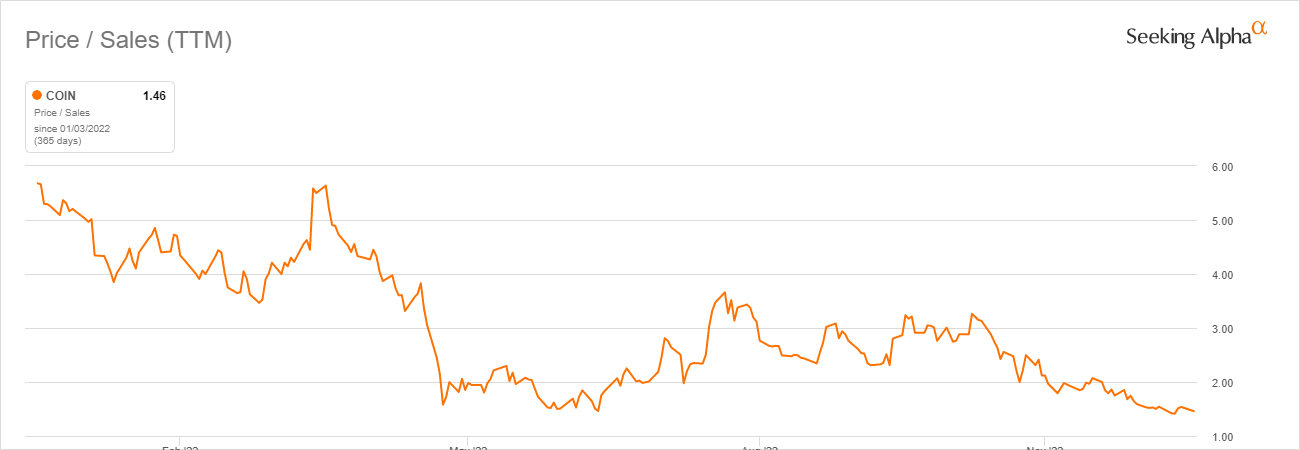

The corporate’s liquid property exceed the long-term liabilities with over $5 billion in money and simply $3.4 billion in long-term liabilities. With a present share value now properly under $40, Coinbase truly is not that costly from a valuation standpoint based mostly on a standard P/S ratio. At 1.46, COIN continues to be close to its all time low value to gross sales ratio of 1.41.

Worth to Gross sales TTM (In search of Alpha)

This costs COIN properly under the sector median value to gross sales ratio of two.84 trailing twelve months. On a ahead trying foundation, the low cost is not fairly as steep with COIN buying and selling at a P/S ratio of two.4 vs a sector median of two.73. The place COIN continues to be overvalued is with trailing value to e-book (1.35) and trailing EV to EBITDA (62.53) – every of that are premiums over sector median with EV/EBITDA being probably the most egregious a number of premium at 411%. This will get us to dangers.

Dangers

There are lots of. The obvious one is that cryptocurrency as an thought may merely be out of gasoline. I do not personally take that view as we have seen these sorts of deep drawdown cycles in Bitcoin (BTC-USD) and within the broader crypto market earlier than. But when crypto is indeed dead within the eyes of the lots and adoption has peaked, then Coinbase is nearly actually in deep trouble as a enterprise and can possible fail to ever ship optimistic earnings once more. That appears to be the most certainly end result in response to the Avenue:

COINBASE GLO 21/31 REGS (Enterprise Insider)

The market clearly has doubts about Coinbase’s capacity to pay its debt obligations. The corporate’s corporate bonds are buying and selling at a really massive low cost to par and at present supply a yield close to 17%. That is with frequent shares which can be down 92% from their peak. Just like the crypto market broadly talking, sentiment in Coinbase is terrible. Coinbase might have a pleasant hoard of money but when the crypto market does not flip round within the subsequent 12-24 months, the corporate may theoretically burn via that money properly earlier than Coinbase has completed paying its debt based mostly on the damaging web earnings figures we have seen in latest quarters.

Abstract

This can be a very contrarian commerce for me. I am a proponent of cryptocurrency however my space of focus is extra within the native property and the miners. I’m very a lot within the camp that individuals ought to self-custody their property. As a centralized change, Coinbase is just not an organization that I’ve a historical past of going lengthy and it is not one thing I’ve advocated buying continuously in BlockChain Reaction. Nonetheless, it’s a platform that I take advantage of as a shopper and one which I’ll proceed to make use of once I purchase digital property earlier than taking custody.

I imagine COIN is priced as if crypto will not get well and I merely do not suppose that is going to occur. In need of the opinion that crypto is all going to zero, I do not see an excellent purpose to promote Coinbase at these ranges. I can not say I adore it as a long-term funding, however as a shorter-term commerce I imagine fortune favors the bulls right here with Coinbase. The elemental thesis may finally favor Coinbase bulls as properly if the U.S. authorities succeeds in making self-custody as troublesome as potential – which is one thing that it appears to be trying based mostly on what’s within the Digital Asset Anti-Cash Laundering Act. AML/KYC rules of the DeFi house is theoretically a tailwind for Coinbase. How that performs out stays to be seen.